As we are entering the fourth year of the presidential cycle, which is more often than not positive for stocks, Wall Street firms have laid out their targets and predictions for 2020. In this post we will review their targets for the S&P 500 as well as highlight some of their opinions regarding 2020.

Before we get into 2020, let’s see what the most accurate and least accurate predictions were for 2019 as it was a challenging year for many. Despite weak global economic fundamentals, a pending trade war and an inverted yield curve, the stock market rallied and made new all-time highs.

Based on the 2019 CNBC Market Strategist Survey, the most conservative forecast last year came from UBS with an S&P 500 target of 2550. Deutsche Bank was the most optimistic with a target of 3250. The S&P 500 ended 2019 at 3230. No less than 16 of the 17 participants in the 2019 CNBC Market Strategist Survey underestimated the markets. Half of those were off by 10% or more. UBS was off by more than 25%.

When considering these forecasts, it is useful to remember what markets were like back in December of 2019. We were in the middle of a major sell off with the S&P bottoming at 2346. As the saying goes, “There is nothing like price to change sentiment”. We tend to be influenced by what happened most recently.

So what do the “experts” think about 2020, after a massive rally in stock markets in 2019?

Well, one could say that Wall Street strategists are cautiously optimistic regarding 2020.

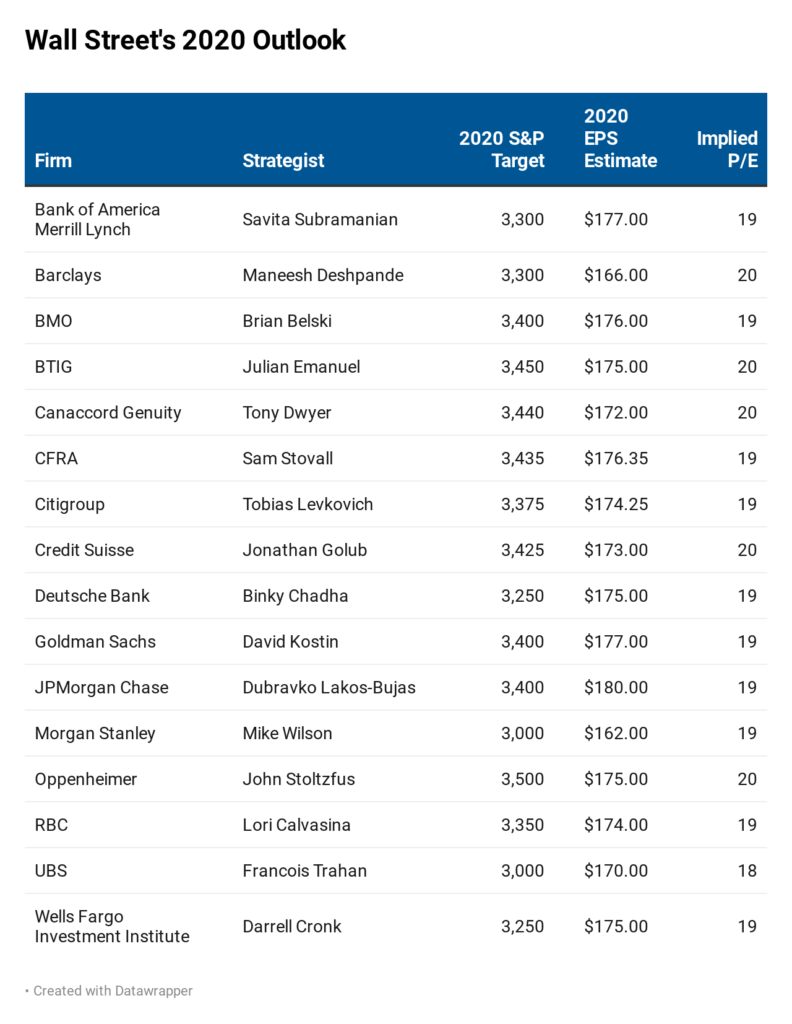

Only two of the sixteen firms surveyed expect negative returns. The highest S&P 500 price target comes from John Stolzfus from Oppenheimer at 3500, implying a 7-8% positive return. UBS and Morgan Stanley are the most concerned, with price targets of 3000, implying an 8% or so decline.

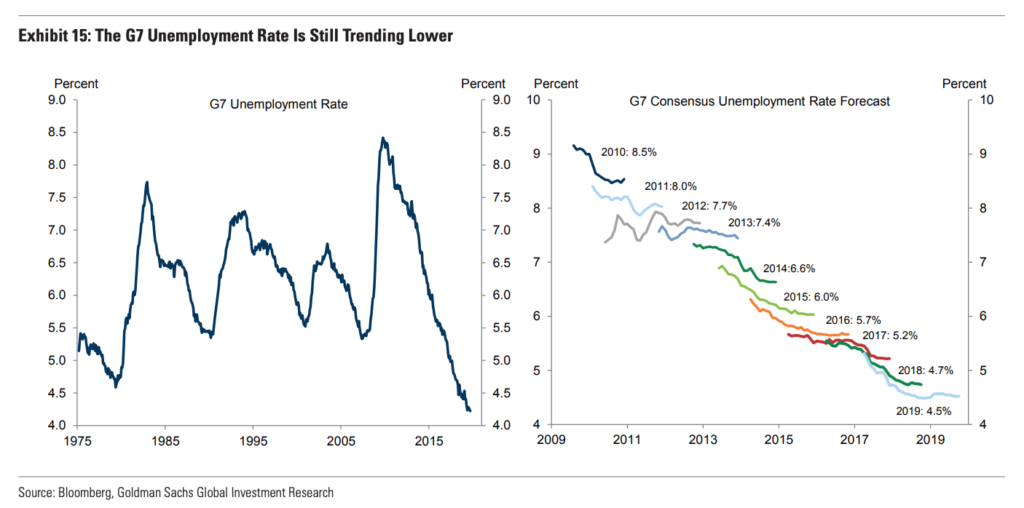

Goldman Sachs expects the consumer to continue to drive the economy as nonfarm payroll growth is expected to stay above the 100,000 breakeven point and the unemployment rate to continue to trend downward. The bank is forecasting unemployment to hit 3.25% by the end of 2020, which it says would be the lowest rate since the Korean War. Wage growth should also rise by about 3.5%. It expects similar trends in other G7 countries.

After delivering three interest-rate cuts this year, the Federal Reserve seemed to indicate that it “would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.” As a result of this, the bank expects fund rates to remain unchanged in 2020.

Goldman identifies the looming presidential election as the single biggest risk to the US economy next year. If one of the four frontrunners for the Democratic nomination does win the general election (Bernie Sanders, Joe Biden, Pete Buttigieg, and Elizabeth Warren), Goldman thinks the federal corporate income tax rate would most likely be upped from 21% back toward 35%. Goldman says it would “reduce S&P 500 earnings in 2021 by 11%” if it were to go all the way back to 35%.

JP Morgan agrees with Goldman Sachs that the consumer will keep driving the economy in 2020: “Part of our optimism for 2020 is based on the continued strength of the US consumer. US consumption is close to its highest share of global GDP since 2008 and consumers are still optimistic, in contrast to US CEOs. Part of the reason: while manufacturing is treading water, service sectors that make up a larger share of the economy are doing better.”

The bank sees two big risks in 2020: “For investors, one 2020 peril is a pickup in US wage or price inflation that indicates that the Fed has made a serious mistake in cutting real rates to zero (again). The Fed’s thinking on policy rates has undergone a massive shift since 2007, with current estimates of the natural real rate of interest at less than 1% (actual real policy rates are even below this level). The other peril: a progressive overhaul of the US economy after the election (bans on stock buybacks, increased corporate tax rates, sector-level collective bargaining, etc.” Reignition of the trade war could be a third headwind.

Recession odds

Most firms including Wells Fargo, UBS, Morgan Stanley and Merrill Lynch, downplay 2020 recession odds but sound cautious about the extent of market growth. Merrill Lynch notes that “The conventional idea of allocating 60 percent to equities and 40 percent to bonds is unlikely to survive into the 2020s” as “today’s bond market “bubble” could become the markets’ biggest vulnerability.”

Real Estate

UBS sees risks in real estate and notes that “Risks in the owner-occupied housing market are elevated in a range of major cities. Investors should seek commercial real estate exposed to long-term trends like e-commerce and rental housing-oriented real estate.”

Goldman Sachs on the other hand states that: “The structural outlook for housing is also strong, as the level of building activity remains well below demographic demand and the homeowner vacancy rate has now fallen to a 38-year low in seasonally adjusted terms.” (!)

Gold

Gold as a diversifier is liked by many Wall Street pundits including ETF provider State Street. UBS is of the opinion that “Gold should outperform more cyclical commodities”.

As the saying goes: “Prediction is very difficult, especially if it’s about the future”. Markets have a way of fooling the most astute investor. Nonetheless, it can be helpful to know what the “big money” is thinking. And… to see who is most often right. We can look back in a year from now to see how all this played out.

The opinions expressed here are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security and should not be construed as recommendations to buy or sell any security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. Any past performance discussed during this program is no guarantee of future results. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Monocot Wealth Management, LLC is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Monocot Wealth Management, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Monocot Wealth Management, LLC unless a client service agreement is in place.

You are now leaving the “Monocot Wealth Management Group” Website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with “Monocot Wealth Management Group” or any advisor(s) whose name(s) appears on this Website. “Monocot Wealth Management Group” is/are independently owned and operated. Schwab neither endorses nor recommends Monocot Wealth Management Group. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with “Monocot Wealth Management Group” under which Schwab provides “Monocot Wealth Management Group” with services related to your account. Schwab does not review the “Monocot Wealth Management Group” Website(s), and makes no representation regarding the content of the Website(s). The information contained in the “Monocot Wealth Management Group” Website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.